Expect denser clusters, not just more plants. Tooling, testing, and special processes will fill gaps around anchors, raising regional capability and lowering variance for everyone in the network.

Automation will get boring—in a good way. Standard stacks, recipe-driven cells, and operator-owned recovery will replace one-off showpieces. ROI will come from uptime, yield, and changeover, not spectacle.

Packaging and reverse logistics will become core competencies. With products built closer to customers, returns and refurbishment will be designed into the flow, turning sustainability into margin.

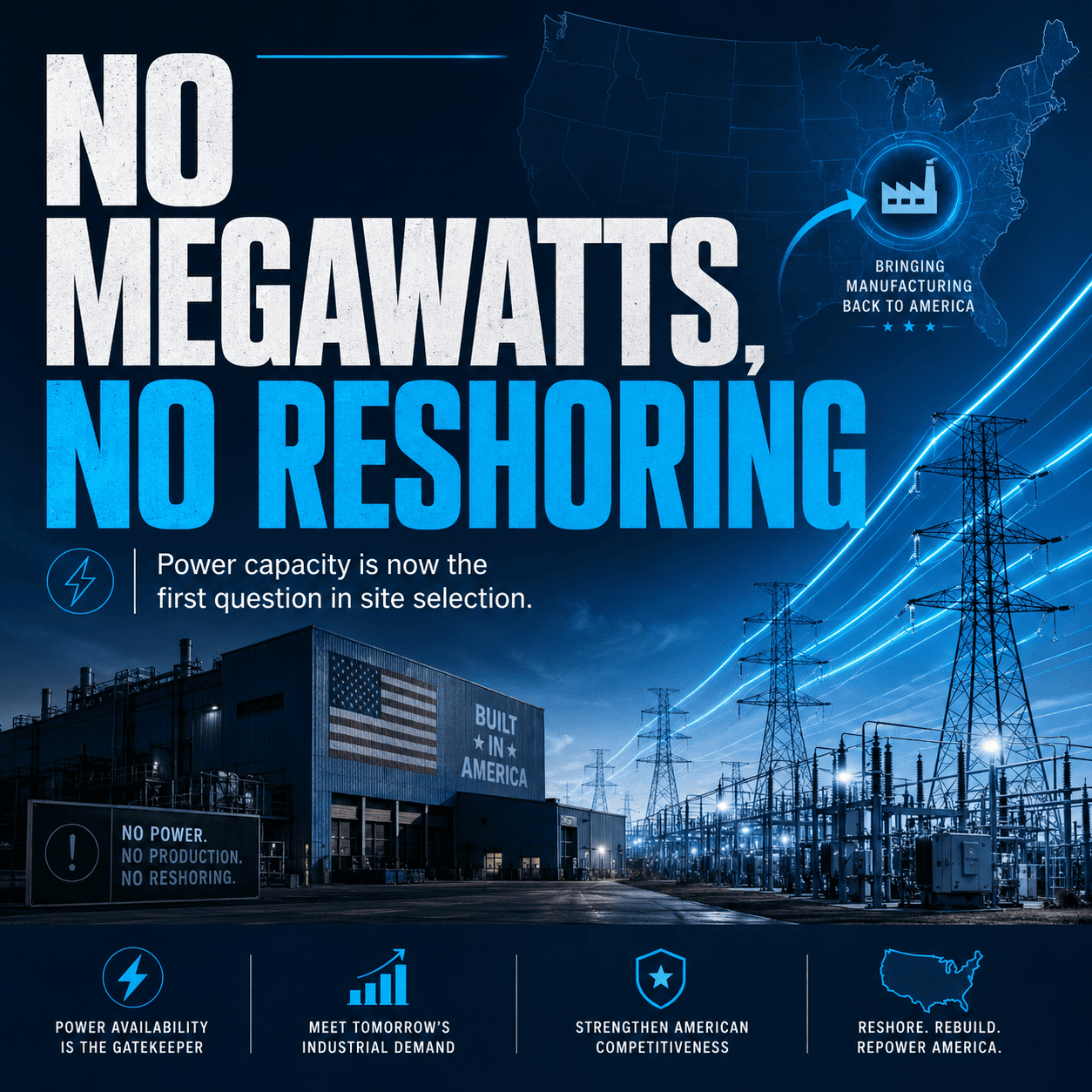

Energy will be a differentiator. Facilities that pair grid reliability with onsite storage and demand control will run steadier and cheaper, and they’ll prove it with data customers can see.

Workforce models will mature. Competency-based apprenticeships, veteran pipelines, and inclusive hiring will be table stakes. Plants that mentor supervisors into coaches will win retention and productivity.

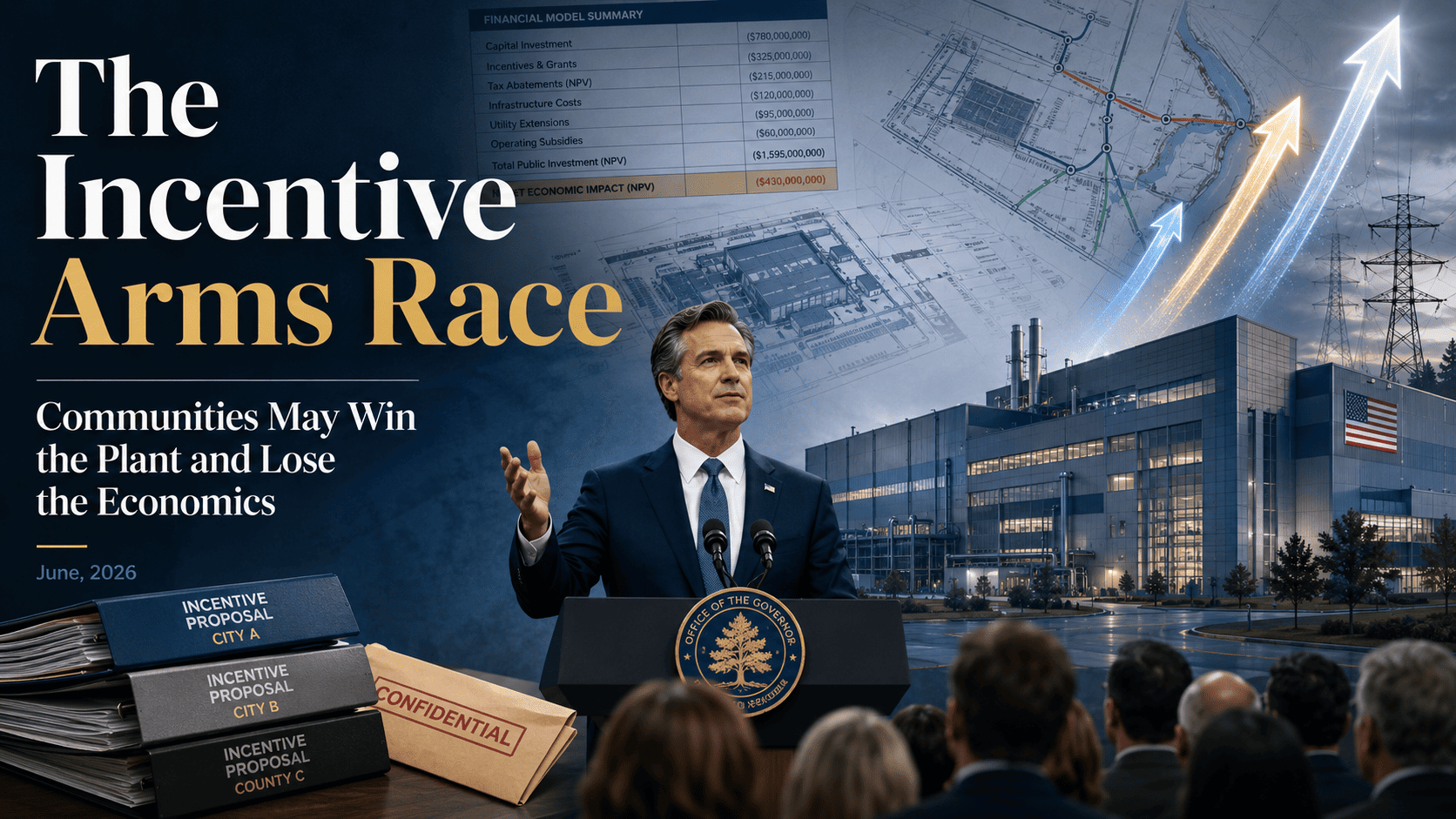

Policy will keep tilting the field. Domestic content rules, training grants, and targeted credits will shape footprints—especially in chips, batteries, medical, and clean tech. The winners will treat policy like a managed workstream.

Data governance will harden. Secure build pipelines, clean lineage for AI, and audited residency will be prerequisites for selling into regulated and enterprise markets. “Where does the data live?” will be a sales question as common as “What’s your lead time?”

Most of all, speed will decide outcomes. Companies that compress time—design to line, order to ship, defect to countermeasure—will take share. Reshoring is the means; responsiveness is the moat.